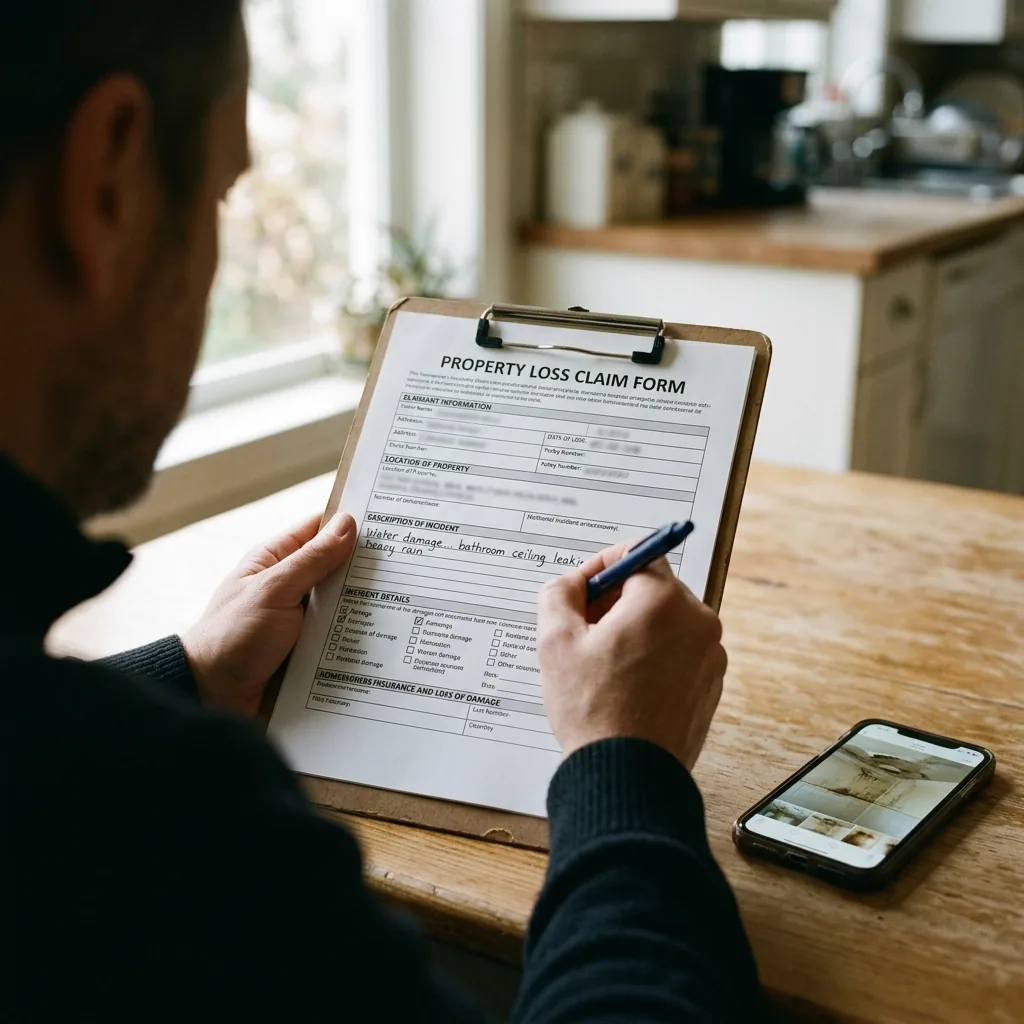

The Claim Isn't Denied for the Reason You'd Think

Homeowners assume a denied water claim means the policy didn't cover the event. Far more often, the event was covered and the claim failed on procedure: no evidence of the original scope, a late notice that let the insurer question the cause, or damaged materials hauled off before anyone official saw them. Each of those is a self-inflicted wound, and each is avoidable if you know it's coming. Think of a claim less as a form to fill out and more as a case to prove.

Mistake One: Cleaning Up Before Documenting

The most expensive misstep happens in the first hour. The instinct is to start hauling wet things out and running fans, but every item you move before the camera comes out is evidence removed from your own case. Walk each affected room with continuous video first, then photograph the source, the waterlines, the ruined flooring and ceilings, and every damaged belonging. Your adjuster verifies the loss from your record of that moment, so build the record before you touch anything.

Mistake Two: Sitting on the Claim

The second mistake is waiting. Most Texas policies require prompt notice, and a delay of several days gives an adjuster a clean opening to argue the damage came from something other than the event you're reporting. File the first notice of loss within 24 hours, even before your documentation is complete. That notice sets the event date and, under Chapter 542 of the Texas Insurance Code, starts the legal clock the insurer now has to answer to.

The Deadlines Your Insurer Has to Meet (Chapter 542)

Once you've filed, Chapter 542 works in your favor. The insurer has 15 business days to acknowledge and begin investigating, 15 business days after receiving your documentation to accept or deny in writing, and 5 business days after acceptance to pay. Blow past any of those and they can owe 18% annual interest on the claim plus reasonable attorney fees. A documented claim filed on time isn't just tidy; it puts a carrier that knows this statute on a schedule it has strong reason to keep.

Mistake Three: Moving Damaged Material Before the Adjuster Sees It

The third mistake looks helpful and isn't. Homeowners tear out wet carpet, drag furniture to the garage, or bag soaked insulation to make the house look better before the adjuster arrives, and in doing so they strip evidence out of the insurer's own field inspection. Document everything in place and leave it until the adjuster has seen it, whether the loss was a slow attic leak or a sudden burst pipe. A restoration company that bills your insurer directly, like our water mitigation service, keeps that documentation in the exact form the adjuster expects.

How to Push Back on a Denial

If the claim comes back denied or light, it's not final. Get the denial in writing with the specific provision cited, then request a re-inspection with your restoration documentation present. When an insurer calls a sudden event "gradual damage" or "maintenance," a licensed public adjuster can review the file and negotiate on your behalf. Texas policyholder law is strong; you just need the evidence ready to use it.

We include full adjuster documentation on every job at no charge. Water damage and a claim to file in Keller? Call (817) 761-5827. Our emergency water damage restoration team walks you through the checklist the moment we arrive, whether you're in Highland Oaks or any other Keller neighborhood.